Comparing Retail and Cost Accounting Methods

Retailers cater to the diverse preferences of consumers with a wider variety of products. Seasonal trends, customer feedback, and market research influence their stock. Many retailers retail vs cost use this strategy as a baseline for pricing strategies, although there’s no hard and fast rule. For example, a retailer might purchase 100 watches from a wholesaler for $20 each.

Business planning

However, if the markup percentage varies greatly, such as 10%, 25% or 40%, then it’s more difficult to use the retail method accurately. The retail inventory method calculates the ending inventory value by totaling the value of goods that are available for sale, which includes beginning inventory and any new purchases of inventory. Total sales for the period are subtracted from goods available for sale.

What Is the Difference Between Selling Price and Cost Price?

For example, a wholesaler might buy 1,000 water bottles from this manufacturer for $2 per bottle. Knowing the difference between wholesale and retail is essential if you want to succeed in ecommerce. Psychological Pricing is a strategy designed to appeal to a customer’s emotional response rather than rational thinking. A common technique is charm pricing, where prices are set just below a round number, e.g., $19.99 instead of $20.

- This costing method is most often used when inventory is perishable and is a favorite for food retailers.

- When entering new markets, it’s important to figure out how much to charge for your products or services.

- So while you might make $2 profit per item, it might cost you more than $2 in overhead to sell that item—in which case you’ll need to adjust your wholesale pricing to make more profit.

- The difference between the price paid and costs incurred is profit.

Set your profit margin

The next step is to add the amounts for each group and divide the result by the number of weighted price categories. Understanding retail pricing is crucial for both consumers and retailers. For shoppers, it offers insights into how much they’re paying above the product’s base cost and why some items are priced higher than others. For retailers, setting the right price is vital to attracting customers, competing with other stores, and ensuring a healthy profit margin. This delicate balance between retail cost and retail price impacts everything from a consumer’s decision to purchase to a retailer’s bottom line. As a catalyst, the wholesale pricing has an undeniable influence on retail pricing.

New approach to selecting KVCs and KVIs

On the other hand, cost accounting gives detailed and accurate inventory values. To calculate the average price that customers pay for products, divide the total sales revenue by the total number of units sold. Wholesale involves selling bulk goods to other businesses at discounted prices.

How do you perform inventory valuation in cost accounting?

In the next section, we’ll explore how leveraging technology can aid retailers in implementing effective pricing strategies, ensuring they remain agile and responsive in a competitive landscape. In conclusion, understanding the impact of wholesale pricing on retail pricing, the role of market conditions and supply chain costs comes in handy. This knowledge lays a solid foundation when setting wholesale prices and helps in predicting the possible pricing trajectory in your retail market. Regardless of the valuation method selected (FIFO, LIFO or weighted average), there will be large differences between cost and retail inventory-valuation methods. Before current efficient computer software, retailers often valued inventory at wholesale, rather than retail, cost. It was impractical to mark inventory to current retail more than once per quarter or annually.

Next, we have the wholesaler’s profit margin, which essentially is their operational cost plus a little extra to ensure their efforts are worthwhile. This too piles up on the total wholesale price, making it a joint culmination of production cost and the wholesaler’s markup. Those companies having a diverse mix of pricing for materials often find the weighted average method most effective. This method multiplies materials cost by the number of pieces on hand. The result is then divided by the number of weighted price categories to arrive at a weighted inventory cost level.

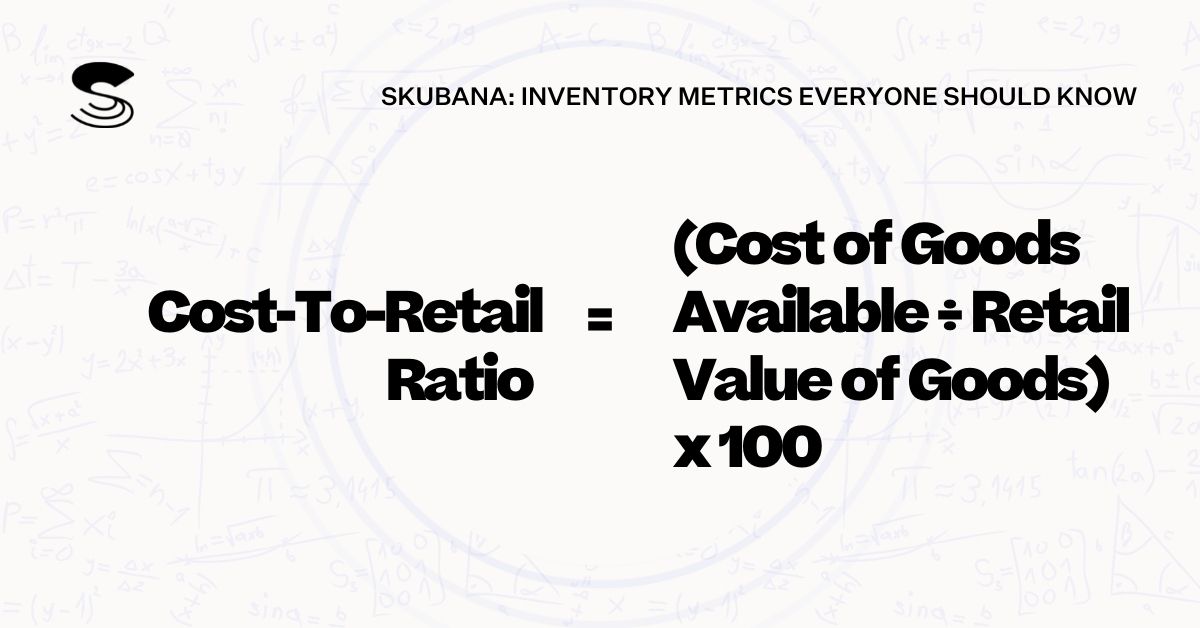

Continue your journey by learning how to account for sales transactions and track COGS efficiently. Using the example above, your inventory was $3,200, total sales were $3,750, and the cost-to-retail ratio was 40%. With the LIFO method, the cost of goods sold would be $90 since the last 20 basketballs you purchased cost $6 dollars each.

The weighted average method of inventory costing is often used when inventory is not perishable but stock can still easily be rotated or intermingled. The FIFO method of inventory costing assumes the first items entered into your inventory are the first items you sell. This costing method is most often used when inventory is perishable and is a favorite for food retailers.

For example, the company has 1,000 pieces at $2 each, 2,000 pieces at $2.75 each, and 4,000 pieces at $3 each. One inventory category equals $2,000, another equals $5,500, and the third equals $12,000. Together they equal an inventory of $19,500, or a value of $2.79 per piece. The retail method calculates the value of ending inventory by adding beginning inventory and any new purchases. The difference is then multiplied by the cost to retail price ratio, which tells you what percentage of the retail price is the cost.